RSUs – How to be as tax efficient as possible

Chris Broome – Chartered Financial Planner

Restricted stock units (RSUs) are a form of employee equity compensation. Essentially, they represent a promise from your employer to grant you shares in the company in the future.

RSUs are especially popular in large tech companies like Microsoft, Amazon, Intel, and Google.

Over time, RSUs can form a significant part of your income and net worth, making it essential to understand how they work, how they’re taxed, and to develop a strategy for managing them effectively.

How Do RSUs Work?

RSUs are awarded to employees at key milestones, such as joining the company, annual performance reviews, or based on company performance. For example, companies like Microsoft and Google often offer RSUs to new hires as part of their onboarding package, as well as during annual reviews.

Two key dates in the RSU process are:

- Grant Date = The date the RSUs are awarded.

- Vesting Date = The date the RSUs can be sold. Vesting typically occurs in tranches over a set period rather than all at once.

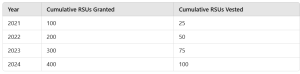

Example Vesting Schedule

Suppose you join Google in January 2021 with a grant of 100 RSUs and a four-year vesting period. Each year, 25% (or 25 RSUs) will vest. If you receive an additional 100 RSUs each year, your schedule might look like this:

How Are RSUs Taxed?

There isn’t a one-size-fits-all RSU tax calculator for UK employees due to the many variables involved, such as your income, how the RSUs are set up, and their vesting schedule. However, here are some general rules:

- Granting = No tax is due when RSUs are granted.

- Vesting = When RSUs vest, they are taxed as income. This includes income tax and employee

National Insurance (NI), and in some cases, employer’s National Insurance (often passed on to the employee).

Example Tax Calculation on Vesting

Let’s say:

- Your annual salary is £100,000.

- Your RSUs vesting this year are worth £25,000.

- You’re liable for both income tax and employer’s National Insurance.

After taxes, you might find that from £25,000 worth of RSUs, only £10,100 remains. Here’s a simplified breakdown:

*Note: The exact amounts may vary based on personal circumstances and tax rates.*

How Can I Reduce Tax on RSUs?

One effective way to reduce RSU taxes is through pension contributions.

Contributing to a pension reduces your adjusted net income, potentially lowering your tax bill and rate.

Avoiding the 60% Tax Trap with Pension Contributions

For example:

- You earn £100,000, and your RSUs worth £25,000 bring your total income to £125,000.

- Because this exceeds £100,000, you enter the “60% tax trap,” where for every £2 above £100,000, your Personal Allowance reduces by £1.

By contributing £25,000 to a pension, your taxable income returns to £100,000, helping you avoid the 60% charge. Here’s how:

Do I Pay Capital Gains Tax on RSUs?

After vesting, you can sell your shares immediately, typically without incurring additional taxes. However, holding shares may lead to capital gains tax on any increase in value from the vesting date to the sale date.

- Capital Gains Allowance = £3,000 per person (2024/25).

- Tax Rates = 20% for higher-rate taxpayers and 10% for basic-rate taxpayers.

Holding shares after vesting means any growth is taxable, while immediately selling shares avoids this.

Minimising Capital Gains Tax on RSUs

Two strategies to reduce capital gains tax:

- Sell Immediately = By selling at vesting, no capital gain applies. You could re-purchase shares in an ISA or SIPP, where future growth is tax-free.

- Transfer to Spouse = Transfer shares to your spouse under the inter-spousal transfer exemption, allowing both of you to use your annual capital gains allowances and potentially reducing the taxable gain.

What Should I Do With My RSUs?

For most people, selling RSUs as they vest is the best approach, reducing the risk and avoiding capital gains tax build up. Holding too much equity in your employer may pose additional risk, similar to investing your cash bonus into the same company.

How Can Longhurst Help?

RSUs are an integral part of your financial picture. At Longhurst, we understand their role within a broader wealth strategy, offering tailored guidance for your RSUs, tax planning, retirement, and investments.

Working with a trusted financial planner can be invaluable in making the most of your RSUs while securing your financial future.

Questions?

Please get in touch if you have any questions about the above or what it might mean for your financial plans.

Please note:

The content of this blog is intended for general information purposes only.

Tax planning is not regulated by the Financial Conduct Authority.